Excited about the potential of blockchain recruiting? You should be. But now let’s get down to brass tacks and harsh truths.

Blockchain—the decentralized ledger technology behind Bitcoin and other cryptocurrencies—is positioned to flip the recruiting industry on its head.

For the uninitiated, blockchain technology promises a new reality where companies can confirm the authenticity of a job applicant’s credentials without having to contact former employers or pay for background checks.

Candidate information stored on a blockchain is both verified by the peer-to-peer network and immune to tampering—a game-changer in a world where up to 85 percent of job applicant resumes contain false information.

In other words, blockchain recruiting promises a lot. The question now is: When will it deliver?

Not anytime soon, if Gartner research is any indication. According to “Predicts 2018: Top Predictions in Blockchain Business” (available to Gartner clients), only 10 percent of enterprise businesses will achieve radical transformation with the use of blockchain technologies through 2022.

In fact, blockchain recruiting will not become a small and midsize business tool until at least 2025, due to factors such as limited resources and a lag in technology awareness compared to their larger brethren.

These predictions aren’t meant to rain on the blockchain parade, and they’re not meant to dissuade you from acting. On the contrary, recruiters that stand idly by and wait for this disruptive technology to reach their doorstep will not be ready to adopt when it’s time.

Here are three key obstacles recruiters should pay attention to before implementing blockchain recruiting in their business, along with tips on how to prepare today for this disruptive technology.

Obstacle #1: Government Entities and Academic Institutions Are Lagging

Think of each ‘link’ in a person’s blockchain-powered job application as a single event in that person’s career. When a person gets a promotion, it’s verified by their employer and added to their blockchain. Performance review? Add it to their blockchain.

That’s the beauty of this technology for recruiters: It’s a single source for verified candidate information. The problem is that there are significant chunks of important candidate information that don’t come from employers.

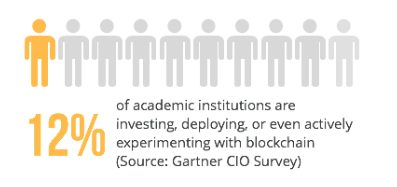

Take a candidate’s college degree(s) for example. Forward-thinkers like Australian University and MIT are currently experimenting with offering graduates digital diplomas powered by blockchain, but it will be a while before the rest of academia catches up:

Then there’s the government. From criminal records to social security numbers, recruiters still rely on government entities for background checks.

And, while the current administration is beginning to consider blockchain in the wake of the Equifax data leak, there are still more than a few regulatory roadblocks, between getting legislation passed and figuring out how to transfer old paper records, before identifiers such as birth certificates start going digital. Sadly, the United States isn’t as agile or forward-thinking as countries such as Estonia, which started adopting blockchain-powered ID cards for its citizens in 2002.

All that to say, it won’t matter how quickly the private sector jumps on the blockchain recruiting bandwagon if other important players in the hiring process lag behind. Until you can get the whole picture of a candidate through blockchain, you should wait to embrace this technology.

Obstacle #2: Legal and Security Concerns Still Exist

In theory, blockchain is an impenetrable record of data. Not only are all transactions on blockchain immutable and irreversible, but to be recorded in the first place, every computing device (or node) on a specific blockchain must agree to the transaction. Short of a nigh-impossible ’51 percent attack’ (where one party controls a majority of the nodes on a specific blockchain), any job candidate information on blockchain is hack-proof.

In practice, however, a number of costly incidents have proven that blockchain isn’t foolproof yet:

- In July 2017, a hacker exploited a flaw in the Ethereum blockchain network and made off with $31 million.

- In January 2018, the largest crypto hack in history on the Japanese cryptocurrency exchange, Coincheck, resulted in a loss of $534 million.

- That nigh-impossible 51 percent attack? It already happened.

Compounding these security concerns are legal ones. What if candidate data logged on a blockchain is incorrect or infringes on someone’s rights? The irreversible nature of blockchain means courts can’t just go in and change the record. Giving legal bodies a skeleton key would also negate one of the key benefits of blockchain: decentralization.

Questions over who has jurisdiction in international transactions are also largely unanswered. If a network in Spain approves a blockchain transaction in the U.S., is it subject to GDPR, the new E.U. data privacy law? Most experts agree blockchain technology and the new law are at odds.

With highly sensitive applicant data on the line, these issues should be addressed before you consider switching recruiting processes over to blockchain.

Obstacle #3: Blockchain Technology Is Expensive

One of the primary reasons businesses are excited about blockchain is the possibility of greatly reducing or even eliminating transaction costs. That’s the main sell for how blockchain recruiting will achieve a positive ROI in the long run: Instead of paying $20 to $30 per candidate for a third-party background check provider, recruiters pay a fraction of that amount to gain access to a candidate’s data themselves.

In order for the numbers with blockchain recruiting to work out positively though, initial costs need to come down. It doesn’t matter if it’s an application purchased through an outside vendor or a proprietary tool built in-house. Simply put, SMBs don’t have the budget for blockchain implementations in their current state, when you consider these three sources of high cost:

3 High Costs Associated With Blockchain Applications

- Finding blockchain talent. Blockchain application developers are rare and expensive, demanding at least $150,000 a year.

- Powering blockchain transactions. Blockchain transactions require a ton of computational power to take place. Cryptocurrency miners currently face high costs largely because of this need.

- Storing blockchain data. Remember, blockchain transactions don’t disappear. As more and more candidate data is added onto a blockchain—even one with a ton of nodes that share the burden of storage—costs will soar.

As a result, 80 percent of blockchain applications done at the enterprise level through 2020 in an attempt to save money will fail to do so, according to Gartner’s Predicts 2018. In order for blockchain recruiting to become feasible for everyone, costs related to the creation and maintenance of these platforms need to fall dramatically.

How You Can Prepare for Blockchain Recruiting Today

Yes, it’ll be a while before blockchain recruiting becomes a tangible reality for your average business. That being said, here are steps you can take right now to prepare for blockchain recruiting:

- Learn more about what blockchain is, and what it isn’t. When companies can simply add the word “blockchain” to their name and see their stock price skyrocket, it’s safe to say there will be more than a handful of software vendors that claim to leverage the technology, but really don’t. Seek out resources and learn more about blockchain to avoid being duped: Gartner is a great source on this topic; so is MIT Technology Review.

- Find alternative solutions in the interim. Here’s an interesting stat: According to Gartner’s “Blockchain Primer for 2018” (available to Gartner clients), 85 percent of projects this year that have “blockchain” in their title will deliver business value without actually using a blockchain. These projects jump-started by the desire to implement blockchain will ultimately arrive at alternative solutions. Instead of waiting around for blockchain to come to fruition, consider a different approach to improve recruiting processes (e.g., switching background check providers).

- Talk to software vendors about their plans for blockchain. Talk with your recruiting software vendor to learn about their plans for blockchain implementations or partnering with other blockchain applications. Oh, and if you don’t have recruiting software, fix that. It’ll improve your organization today and suitably prepare it for the tech of tomorrow.

Want to learn more about how software and technology can improve recruiting processes and hiring outcomes? Check out more helpful articles on Software Advice.